TitleUnderstanding Digital Currency: Characteristics and Imp

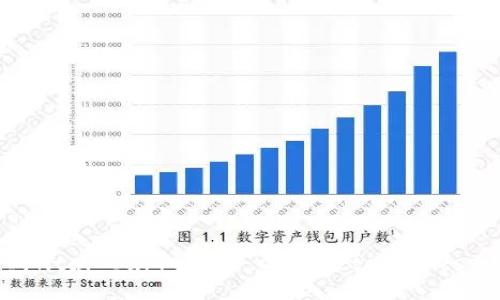

Digital currency refers to any form of currency that is available only in digital form, as opposed to physical banknotes and coins. It has gained significant traction in recent years, leading to a growing interest from individuals, businesses, and governments around the world. Understanding digital currency includes exploring its various forms—such as cryptocurrency, central bank digital currencies (CBDCs), and stablecoins—along with their unique characteristics that differentiate them from traditional fiat currencies.

This detailed examination will cover the main features of digital currencies, their underlying technologies, their advantages and disadvantages, and the future prospects of this rapidly evolving field.

### Characteristics of Digital Currency #### 1. **Decentralization**One of the most striking features of digital currencies, particularly cryptocurrencies like Bitcoin and Ethereum, is decentralization. Unlike traditional currencies governed by central banks, cryptocurrencies operate on blockchain technology, which allows for a peer-to-peer network without a central authority. This decentralized nature reduces the reliance on banks and intermediaries, empowering users to have greater control over their funds.

Decentralization provides advantages such as increased resilience against systematic failures and censorship, as no single entity can dictate terms or control transactions. However, it also implies that there is no central authority to enforce regulation or protect consumers, which can pose risks.

#### 2. **Anonymity and Privacy**Many digital currencies offer varying degrees of privacy and anonymity, which is attractive to users concerned about surveillance and data breaches. Cryptocurrencies often use cryptographic techniques to obscure user identities and transaction details. While Bitcoin transactions are traceable on a public ledger, other cryptocurrencies like Monero and Zcash are designed to prioritize user anonymity.

This characteristic raises significant concerns regarding illegal activities, such as money laundering and tax evasion, prompting discussions about the need for regulation in the digital currency space. Balancing privacy with the need for transparency is an ongoing challenge in this field.

#### 3. **Immutability**Transactions made using digital currencies are recorded on a blockchain, which is a digital ledger that is immutable once information is added. This means that once a transaction is confirmed and added to the blockchain, it cannot be altered or deleted. As a result, it guarantees a certain level of security and trust in the transaction process.

Immutability is advantageous for maintaining accurate financial records and preventing fraud. However, it also poses challenges for resolving disputes or correcting errors, as there is no straightforward way to reverse transactions.

#### 4. **Accessibility**Digital currencies offer increased accessibility compared to traditional banking systems. Anyone with an internet connection can participate in the digital currency ecosystem, allowing for greater financial inclusion, especially in underbanked regions of the world. Additionally, the frictionless nature of digital currency transactions enables instant global payments, simplifying cross-border transfers.

However, accessibility also comes with challenges, such as the need for knowledge about how to use wallets and exchanges. Technological barriers can hinder some users from fully engaging in digital currency transactions.

#### 5. **Volatility**Digital currencies, especially cryptocurrencies, often exhibit high volatility compared to traditional currencies. Price fluctuations can be dramatic, influenced by factors such as market sentiment, regulatory news, and technological developments. This volatility creates both investment opportunities and risks, as traders and investors may experience significant gains or losses over short periods.

While some proponents argue that volatility is a characteristic of a nascent market that could stabilize over time, critics warn that it undermines the potential for digital currencies to serve as a stable medium of exchange.

### Future Prospects of Digital CurrencyThe future of digital currency is uncertain yet promising. Advances in blockchain technology, increasing acceptance by mainstream financial institutions, and the potential for regulatory frameworks will shape the evolution of digital currencies. Furthermore, the emergence of Central Bank Digital Currencies (CBDCs) signals a shift in how governments perceive and interact with digital forms of money.

CBDC projects are aimed at combining the advantages of digital currencies with the stability and regulatory support of traditional fiat currencies. Countries like China, Sweden, and the Bahamas are at the forefront of these initiatives, experimenting with digital currency systems that could redefine monetary policy and financial systems globally.

The growing convergence of finance and technology, highlighted by the rise of fintech, will also play a crucial role in the landscape of digital currencies, fostering innovation and creating new opportunities for user engagement and interactions.

--- ### Frequently Asked Questions #### 1. **What is the difference between cryptocurrencies and stablecoins?**Understanding the Distinction

Cryptocurrencies and stablecoins are both types of digital currencies, but they are designed to serve different purposes and have distinct mechanisms of operation. Cryptocurrencies, such as Bitcoin and Ethereum, are primarily decentralized and operate on a blockchain technology without any backing from tangible assets or fiat currencies. As a result, their prices are prone to significant fluctuations influenced by supply and demand dynamics, investment speculation, and market sentiment.

Stablecoins, on the other hand, aim to provide the stability of traditional currencies while retaining the advantages of digital currencies. They are pegged to stable assets, commonly fiat currencies like the US dollar or the Euro, or commodities like gold. This pegging mechanism helps to minimize volatility, providing users with a predictable value for transactions.

One common stablecoin is Tether (USDT), which aims to maintain a value equal to one US dollar. There are also algorithmic stablecoins like Ampleforth (AMPL), which adjust the supply of the token based on the current price in the market.

While cryptocurrencies may be viewed as speculative assets, stablecoins are often used in decentralized finance (DeFi) applications to facilitate lending, trading, and other financial services without incurring the risks associated with price volatility. This makes stablecoins appealing for everyday transactions or as a means of preserving value.

#### 2. **What role do regulatory bodies play in the digital currency ecosystem?**The Importance of Regulation

Regulatory bodies play a critical role in the digital currency ecosystem by establishing frameworks that govern the use of digital currencies and protect consumers. As digital currencies have gained prominence, regulators worldwide have sought to address various challenges, including security, fraud prevention, and market integrity. The lack of regulation has allowed for rampant scams and theft, contributing to concerns among potential users and investors.

Regulatory approaches vary by country. Some nations, like the United States, take a more cautious approach, advocating for measures to prevent illegal activities, such as money laundering and tax evasion, without stifling innovation. The Financial Action Task Force (FATF) has proposed guidelines for countries to implement Know Your Customer (KYC) and Anti-Money Laundering (AML) standards for digital asset services.

Other countries, like China, have been more aggressive in their stances, outright banning cryptocurrencies and focusing on the development of Central Bank Digital Currencies (CBDCs) to maintain control over their financial systems.

The regulatory landscape will undoubtedly influence the development of digital currencies and adoption rates, as clear regulations can protect consumers while fostering innovation and mainstream adoption. Striking a balance between regulation and facilitating a thriving ecosystem will be essential for the longevity of digital currency.

#### 3. **How does blockchain technology underpin digital currency?**The Foundation of Digital Currency

Blockchain technology serves as the backbone of digital currencies, providing the necessary infrastructure for their operation. A blockchain is a distributed ledger technology that records transactions across thousands of computers in a network, ensuring transparency, security, and immutability.

When a transaction occurs, it is grouped with other transactions into a block. Once verified by network participants (nodes), this block is added to the existing chain, creating a chronological record of transactions that cannot be altered. This process relies on consensus mechanisms such as Proof of Work (PoW) or Proof of Stake (PoS) to secure the network and validate transactions, reinforcing trust without requiring central authorities.

In addition to supporting cryptocurrencies, blockchain technology has numerous applications across various sectors, including supply chain management, healthcare, voting systems, and digital identity verification. Its use in digital currencies exemplifies its potential for enhancing security, reducing costs, and increasing efficiency in financial transactions. As technology continues to evolve, so too will its applications within the ecosystem, signaling a new era for global finance.

#### 4. **What are the security concerns associated with digital currencies?**Addressing Security Risks

While digital currencies offer innovative features and advantages, they are not without risks, particularly concerning security. One primary concern is the vulnerability of digital wallets, which store users' private keys and their digital assets. If a wallet is compromised, a user can lose their funds without any recourse, as the nature of decentralized currencies means that transactions are irreversible.

Additionally, exchanges and trading platforms are prime targets for hackers due to their concentrated holding of digital assets. Various high-profile hacks have led to the loss of millions of dollars, raising questions about the safety of funds held on these platforms. Users must choose reliable and secure exchanges that implement robust security measures, such as multi-factor authentication and cold storage for assets.

Another concern is the potential for phishing scams and malware attempts aimed at tricking users into giving away sensitive information. Educating users about secure practices, such as verifying URLs, avoiding suspicious links, and using hardware wallets, is crucial for minimizing risks.

Regulators and industry stakeholders are continually working to improve security frameworks, but user awareness and proactive measures remain vital for protecting digital currency investments.

#### 5. **How can digital currencies contribute to financial inclusion?**The Potential for Financial Empowerment

Digital currencies have the potential to significantly enhance financial inclusion, particularly for unbanked and underbanked populations around the world. An estimated 1.7 billion adults remain without access to traditional banking services, primarily due to geographical constraints, costs associated with banking, and lack of identification documents. Digital currencies can offer solutions to these barriers by providing accessible financial services through smartphones and the internet.

With digital wallets and applications, individuals can create accounts without the need for traditional banking infrastructure. This accessibility empowers users to engage in financial transactions, send and receive payments, and even save in a digital format, all without needing a bank account.

Moreover, digital currencies can facilitate remittances, allowing individuals to send money across borders at lower fees and faster speeds compared to traditional remittance services. This ability is particularly vital for migrant workers who frequently remit funds back to their families.

Enabling financial inclusion through digital currencies also has broader economic implications, as it fosters entrepreneurship and innovation in underserved communities. However, for this potential to be realized, continued efforts are required to address issues such as technological literacy, access to the internet, and the development of user-friendly applications.

--- ### ConclusionThe realm of digital currency is rapidly evolving, presenting challenges and opportunities for individuals, businesses, and governments alike. Understanding its characteristics, implications, and the transformative potential it holds is crucial for navigating the future of finance. As we explore these technological innovations, the debate surrounding regulation, security, and financial inclusion will undoubtedly shape the landscape of digital currencies in the years to come.